Specialty Lending's KYC, AML & Fraud Challenge: Why Fragmented Tools Fail

WRITTEN BY

Specialty lending is scaling fast. Invoice financing, equipment leasing, merchant cash advances, and asset-based lending all grew as traditional banks retreated from complex deals. But growth brings scrutiny. FinCEN is watching. Regulators now expect bank-grade KYC, AML monitoring, and fraud controls, even from non-bank lenders serving SMB lending and commercial finance. One study estimates that financial crime compliance now costs U.S. and Canadian financial institutions roughly $61 billion a year, with 99% of firms reporting rising spend.

The problem? Most specialty lenders inherited a compliance stack that wasn't designed for their business. It accrued over time: a KYC provider here, a document verification tool there, AML screening from a third vendor, fraud scoring from a fourth. Each tool works in isolation. When a complex deal hits, cross-border transactions, layered ownership, high-value equipment leases, the gaps become obvious.

Why Specialty Lending Faces Distinct KYC, AML, and Fraud Risk

Specialty lending isn't 'small business loans.' It covers invoice factoring, asset-based lending, equipment finance, and merchant cash advances. Each product has unique risk patterns that generic compliance software isn't designed to handle.

Complex Customer Structures

Traditional lenders verify individuals. Specialty lenders verify businesses, often with multi-layered ownership, special-purpose vehicles, or beneficial ownership buried within holding companies. Know Your Business (KYB) becomes as critical as KYC, but most identity verification platforms are designed for consumer finance, not commercial structures.

Asset-Specific Fraud Schemes

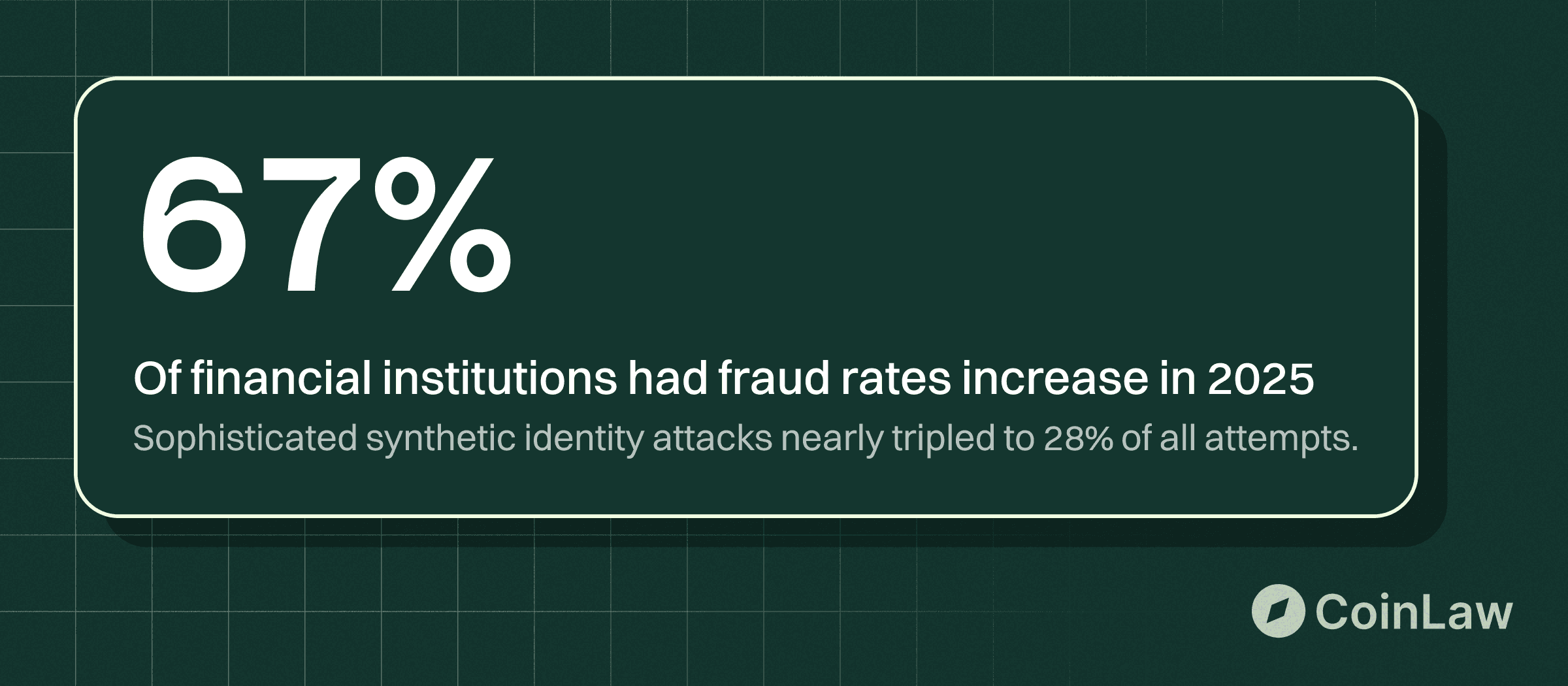

In invoice financing, fraud isn't just synthetic identity fraud or identity theft, it's double-pledging receivables to multiple lenders or financing invoices that don't exist. In equipment leasing, it's financing stolen assets or ghost inventory. In merchant cash advances, it's fabricated revenue statements. Each scheme requires different fraud detection signals, but most tools only catch basic identity manipulation. Recent synthetic identity fraud research found that fraud rates increased at 67% of financial institutions in 2025, and the share of sophisticated attacks nearly tripled to 28% of attempts, exactly the kind of evolving behavior static rules struggle to catch.

Speed vs. Risk Tradeoffs

Specialty lending clients expect fast capital. They're growth-stage businesses that need funding this week, not next quarter. That urgency creates pressure to approve quickly. But fraudsters exploit exactly that pressure. Without intelligent risk-based decisioning, teams either slow everyone down with manual review or let risky deals through.

Regulatory Expectations Are Rising

Non-bank lenders used to operate with lighter oversight. Not anymore. FinCEN and state regulators now expect Customer Identification Programs (CIP), ongoing AML monitoring, and documented fraud prevention programs. According to industry data, financial institutions spend 3-5% of annual revenue on AML compliance alone. For specialty lenders without centralized infrastructure, that cost is even higher. FinCEN has gone so far as to launch a dedicated survey of AML/CFT compliance costs for non-bank financial institutions because those expenses, often intertwined with fraud monitoring, have become material on their own.

Where Fragmented KYC, AML, and Fraud Tools Break Down

Most specialty lenders didn't intentionally design their compliance stack ... the stack accumulated. A basic KYC tool for onboarding, an AML screening service for watchlist checks, a fraud score from a credit bureau, maybe a document verification API. Each vendor works in isolation. The result is a system with three structural problems.

No Shared Context Across Checks

When identity verification, AML screening, and fraud detection live in separate tools, no single system sees the full picture. Your KYC provider verifies the business name and beneficial owners. Your AML tool flags a Politically Exposed Person (PEP) match. Your fraud score shows recent credit inquiries. But none of these tools communicate with each other, natively. Analysts and developers manually stitch together the data together in a spreadsheet or in a custom developed environment, introducing delay and error. In fast-moving specialty lending deals, that delay costs approvals.

Static Rules in a Dynamic Threat Environment

Most fraud detection tools apply fixed rules: if the fraud score is above X, approve; below Y, decline. But synthetic identity fraud schemes, document fraud, and first-party fraud evolve constantly. Static rules lag reality. As new attack patterns emerge - deepfake documents, AI-generated identities, coordinated loan stacking, yesterday's thresholds fail. Without intelligent machine learning models, teams either tighten controls and reject good customers or loosen them and absorb fraud losses. In a recent Federal Reserve-cited survey, nearly four in ten financial institutions said synthetic identity fraud is now a persistent or growing problem, with mule accounts emerging as a major driver of losses.

Manual Review as the Default Fallback

When tools conflict in their responses, the case lands with an analyst. At scale, manual review queues become unmanageable. Compliance teams spend hours reconstructing decisions from fragmented data. When regulators ask how a risky deal was approved, there's no clear audit trail. Decisions live in email threads and spreadsheets, not in governed risk workflows.

Why Specialty Lenders Attempt to Build Custom Compliance Workflows

Faced with fragmentation, many specialty lenders consider building their own compliance platform. The logic seems sound: 'Our business is unique. Off-the-shelf tools don't fit. We'll own the system and control the roadmap.'

"Our Process Is Different." Invoice financing requires verifying receivables and debtor creditworthiness. Equipment leasing needs asset condition checks and title verification. Merchant cash advances demand bank statement analysis. Each product has unique data requirements that don't map to consumer-focused KYC tools. Teams conclude that only a custom-built workflow can capture that nuance.

Perceived speed, cost, and control. Building in-house feels faster than procuring a platform. It promises direct control over every rule, threshold, and integration. No vendor dependencies. No waiting for feature requests. Just your team, your code, your roadmap.

Vendor fatigue and fear of lock-in. After cycles of 'magic' fraud tools that promised one-click protection but delivered high false positives and manual review backlogs, teams are skeptical. They worry that adopting another platform means locking into a single vendor's design choices. Building in-house feels like reclaiming control.

The Hidden Cost of Building Compliance Infrastructure In-House

Custom-built compliance workflows rarely fail overnight. They erode slowly as fraud tactics evolve, transaction volume grows, and regulatory expectations tighten. The costs show up in three areas.

Engineering bottlenecks and technical debt. Every new fraud scheme, data source, or regulatory requirement becomes a development ticket. Add a rule for synthetic identity detection. Integrate a new AML screening API. Adjust thresholds for PEP matches. Releases are batched, QA is stretched, and fixes trail incidents by months. Meanwhile, identity verification logic becomes entangled with core lending systems. Only a few engineers understand it, creating a bottleneck for every compliance change.

Exception sprawl and inconsistent decisions. As volume grows, edge cases multiply. Cross-border transactions, complex ownership structures, and new product lines. Each exposes gaps in the original design. Local teams patch with one-off rules and manual overrides. Decision logic diverges across regions and products. When regulators audit, they find inconsistent KYC and AML practices that are difficult to defend.

Operational drag and compliance team burnout. When code lags reality, manual review fills the gap. Analysts spend hours reconstructing decisions from emails, PDFs, and screenshots. Cost per application rises. Error rates climb. Attrition follows. The compliance team that should be refining the fraud prevention strategy is instead firefighting operational chaos.

Regulatory exam pain and remediation cost. Examiners expect documented KYC and AML programs, clear risk-based decisioning frameworks, and evidence that policies are applied consistently. Custom workflows stitched across lending platforms, document verification tools, and spreadsheets often fail that test. Findings trigger remediation projects that look suspiciously like the comprehensive platform investment teams tried to avoid.

How Orchestration Changes Compliance Speed, Risk, and Scalability

Orchestration isn't a buzzword; it's a structural choice. It means treating identity verification, KYC, AML screening, and fraud detection as one coordinated system rather than disconnected point checks.

Single decision logic across channels. Instead of hard-coding different compliance workflows into each product, orchestration platforms centralize rules. Invoice financing, equipment leasing, and merchant cash advances all call the same decision layer, with controlled variations where risk justifies them. This ensures consistent KYC, AML, and fraud checks across the portfolio.

Layered, risk-based controls. Orchestration makes it straightforward to define low-, medium-, and high-risk paths. Low-risk applicants with clean KYC and fraud scores: auto-approve. Medium-risk cases trigger additional document verification or Enhanced Due Diligence (EDD). High-risk profiles might leverage PEP matches, synthetic identity flags, or cross-border transactions and end by routing to expert review. This tightens scrutiny on real threats while avoiding blanket friction.

Faster iteration with measurable impact. When KYC, AML, and fraud logic live in a configurable decision layer, compliance teams can adjust policies and see the impact on fraud rates, approval speed, and customer experience. The organization moves from reactive patches to governed experimentation.

Clearer audit trail and governance. An orchestration platform records which checks ran, what signals were returned, what rules fired, and why a case followed a specific path. That traceability underpins internal model governance, supports regulatory exams, and provides a factual basis for tuning fraud controls.

What Buying Orchestration Enables for Specialty Lenders

Once a team accepts that orchestration is necessary, the build-vs-buy decision becomes sharper. Buying orchestration doesn't remove responsibility. It changes where you spend effort.

Faster deployment of better controls. Integrations to KYC providers, AML screening services, fraud detection tools, and credit bureaus are standardized once and reused across products. This reduces time-to-value when adding or swapping data sources.

Policy-driven change instead of code-driven change. Compliance teams can propose and test rule changes inside a defined framework, reducing dependence on engineering while still operating within technical guardrails.

Stronger oversight of partners and channels. Shared decision logic and visibility into application behavior make it feasible to spot outliers and demonstrate to supervisors that KYC, AML, and fraud risks are managed consistently across the business.

For identity, fraud, and data partners: Cleaner integration stories. KYC providers, document verification tools, and fraud scoring vendors can plug into orchestrated flows as components instead of trying to own end-to-end journeys.

The Real Build-vs-Buy Question for Specialty Lenders

Most leadership teams discover that the real build-vs-buy question isn't about any single KYC tool or fraud score. It's about the orchestration layer itself. Connecting identity verification, AML screening, document verification, and fraud detection often proves more expensive than anticipated. The cost shows up in time, opportunity cost, and regulatory risk.

Partnering for orchestration lets specialty lenders put their energy into strategy, policy, and customer relationships, while still maintaining the level of control regulators and boards expect over KYC, AML, and fraud decisions.